")

How to File Corporate Tax in UAE Step by Step

If this is your first time filing corporate tax in the UAE, you're not behind. You're just early in a process most business owners are still getting used to.

The 28th comes around every month or quarter. For every VAT-registered business in the UAE, it means the return is due. EmaraTax guides you through each section. The errors happen in the detail.

The VAT filing process in UAE runs in seven steps. Errors rarely happen in those steps. They happen earlier: in how supplies are classified, which invoices qualify, and whether the Input VAT you plan to claim is recoverable.

Nothing here replaces qualified tax advice. For your specific situation, speak to a UAE tax professional.

Every VAT return comes down to two numbers:

Output VAT: tax you collected from customers

Input VAT: tax you paid on purchases

The FTA takes the net difference. You either owe the balance or have a refund to claim.

Both go on Form VAT 201 through EmaraTax.

Do You Need to Register & File?

Check your taxable supplies and imports over the past 12 months against the official UAE VAT registration thresholds:

Mandatory for above AED 375,000: You must register and file a return for each Tax Period.

Voluntary for AED 187,500 to AED 374,999: You may choose to register and file.

Not required for below AED 187,500.

If you are registered under either threshold, the VAT 201 return is a legal obligation for each Tax Period.

The VAT filing process in UAE runs in seven steps. No step can be skipped without affecting the accuracy of the one that follows.

Collect all Tax Invoices issued and received during your Tax Period.

Separate standard-rated, zero-rated, exempt, and out-of-scope supplies into distinct records.

Total your Output VAT from sales and your recoverable Input VAT from purchases.

Log into EmaraTax and open your VAT account dashboard.

Select Form VAT 201 and enter your Output VAT, Input VAT, and any adjustment figures.

Review the net payable amount and confirm all entries are correct.

Submit the return and pay the balance due. Payment must clear by the 28th, not just leave your account.

Supply classification is where most Input VAT errors begin. The category you assign to a supply changes not just what you report as Output VAT, but what you are allowed to claim back.

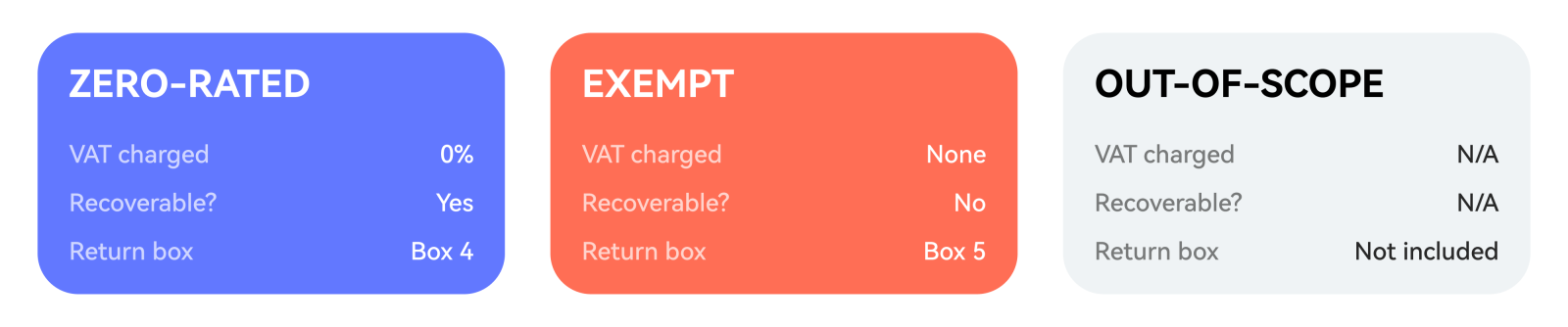

Zero-rated supplies are taxable at 0%. No VAT is charged to the customer, but Input VAT on related business costs is fully recoverable. The most common examples are international exports of goods, certain healthcare and educational services, and some international transport; these go in Box 4 of the VAT 201.

Exempt supplies work differently. No VAT is charged, and Input VAT on costs directly linked to exempt activities cannot be recovered. Certain financial services, bare land, and residential property (in specific circumstances) fall into this category and go in Box 5.

With mixed taxable and exempt income, a partial exemption calculation determines how much of your Input VAT is actually recoverable.

Out-of-scope supplies, such as dividends or salaries, are not VAT transactions and do not appear on the return.

Misclassifying an exempt supply as zero-rated inflates your Input VAT claims. It is one of the most common reasons the FTA opens an audit.

The FTA assigns your Tax Period, either monthly or quarterly, based on annual taxable turnover. You can request the FTA for a change to your tax period, and in practice, most reasonable requests are approved.

File and pay by the 28th day of the month following your Tax Period. The same rule applies to both period types.

Monthly filers: January Tax Period, deadline 28th February.

Quarterly filers: January to March Tax Period, deadline 28th April.

If the 28th falls on a weekend or public holiday, the next working day applies under Federal Decree-Law No. 8 of 2017. The VAT return deadline UAE for 2026 follows this same rule. File and initiate payment early. VAT transfers require processing time and a payment sent on the day may not clear in time.

Three errors account for most UAE VAT filing mistakes: invalid Input VAT claims, supply misclassification, and a missed 28th.

Late filing costs AED 1,000 the first time. A second offense within 24 months doubles that to AED 2,000. Late payment adds a further penalty of 14% per annum on the overdue amount, charged monthly. Even a one-day delay into a new month triggers that month's charge.

Errors found after submission can be corrected through an FTA Voluntary Disclosure, filed directly through EmaraTax. The FTA treats self-reported corrections differently from errors found during an audit. Disclosing first means lower penalties.

If the error affects your tax liability by AED 10,000 or more, a Voluntary Disclosure is required within 20 business days of discovering it. Below that threshold, the correction can be included in your next VAT return instead. Either way, check the late VAT payment penalty UAE rules under Cabinet Decision No. 129 of 2025.

Questions About the UAE VAT Filing Process

How do you file a VAT return in the UAE?

Log into EmaraTax and open Form VAT 201 for your Tax Period. Enter your Output VAT and Input VAT figures. Then, confirm the payable amount and submit.

How long must you keep UAE VAT records?

UAE VAT law requires records to be kept for a minimum of 5 years. If your business is also subject to Corporate Tax, that extends to 7 years. When both apply, default to 7.

Do you need to pay VAT before filing the return in UAE?

Filing and payment share the same deadline: the 28th day of the month following your Tax Period. Your payment must clear by that date, not just leave your account. Build bank processing time into your schedule.

Can you claim Input VAT on all your business expenses?

No. Input VAT is only recoverable where the related supply is taxable and the expense has a direct business purpose. Exempt-related costs, most entertainment expenses, and certain motor vehicles are blocked or restricted under UAE VAT law.

If this is your first time filing corporate tax in the UAE, you're not behind. You're just early in a process most business owners are still getting used to.

VAT in Dubai is exactly 5%. One rate, applied uniformly across all seven emirates. No exceptions by location. But how much is VAT in Dubai as a business owner i...

Dubai has a well-earned reputation for zero personal income tax. Corporate tax tells a different story. The UAE introduced a 9% corporate tax rate in 2023, appl...

Download the app and make your everyday

life more efficient*

* coming in late 2026