How Much Is VAT in Dubai? Understanding the UAE’s 5% Tax System

VAT in Dubai is exactly 5%. One rate, applied uniformly across all seven emirates. No exceptions by location. But how much is VAT in Dubai as a business owner i...

Dubai has a well-earned reputation for zero personal income tax. Corporate tax tells a different story. The UAE introduced a 9% corporate tax rate in 2023, applied not to revenue but to taxable income. How to calculate corporate tax in UAE correctly starts with that distinction. The taxable income figure comes from net accounting profit after a set of legal adjustments, and each one shapes your final bill.

Accounting profit is your total revenue minus all business expenses for the period, prepared under standard financial reporting rules. The Federal Tax Authority (FTA) does not tax that number. It taxes taxable income.

Taxable income is accounting profit after adjustments: non-deductible expenses added back in, exempt income removed. That final figure is what the rate applies to.

The rate structure has two bands. Taxable income up to the AED 375,000 threshold is taxed at 0%. Any amount above that figure is taxed at 9%.

Only the portion exceeding the threshold carries the 9% charge. A business with AED 500,000 in taxable income pays 9% on AED 125,000 only, not the full amount.

Before running any numbers, check your position:

Natural person with annual turnover below AED 1 million? Corporate tax does not apply.

Revenue at or below AED 3 million for the taxable period? You may qualify for Small Business Relief and owe nothing.

Registered as a Qualifying Free Zone Person (QFZP)? A 0% rate may apply to your Qualifying Income.

Taxable income at or below AED 375,000? The 0% rate applies across this full band.

If none of these apply to your business, the calculation proceeds with the four-stage formula below.

Four stages determine how to calculate corporate tax in UAE. Each builds on the result of the last.

Your financial statements give you the first number. The FTA's rules then govern what adjustments apply, what reliefs reduce the figure, and what rate runs against what remains.

Accounting profit is the starting point

Your starting point is the net accounting profit from your financial statements, prepared under IFRS or IFRS for SMEs. This is revenue minus all business expenses. It is not your cash balance.

That figure is not yet your tax base. It needs adjustment first.

Taxable income adjustment

Tax adjustments bring accounting profit in line with what the FTA actually taxes. Non-deductible expenses are added back. Exempt income is removed. What remains is the taxable income.

Before the rate applies, one more check: whether any reliefs or prior losses reduce that figure further.

Reliefs or Carried-Forward Losses

Eligible businesses can reduce taxable income before the rate applies. Small Business Relief, where claimed, may bring liability to zero. Losses from a prior taxable period may also offset current profits, subject to FTA conditions.

Once taxable income is confirmed, the rate is the final step.

UAE Corporate Tax Rate

Apply 0% to the first AED 375,000. Apply 9% to everything above. Add both figures. That total is the liability for the taxable period.

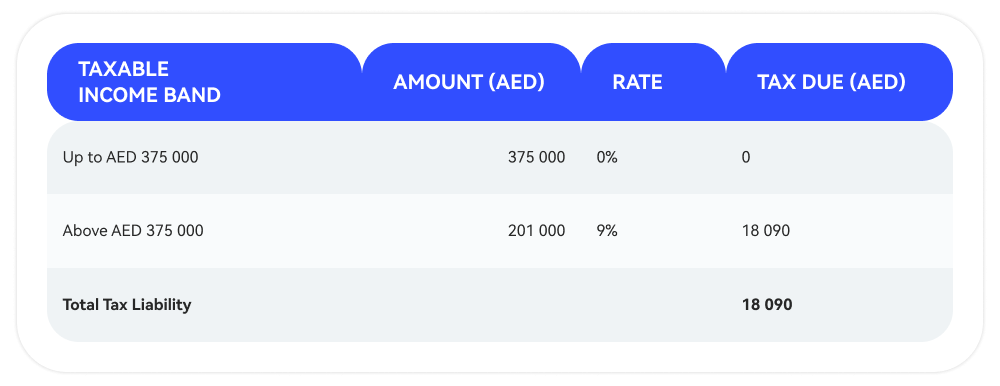

A small IT services firm in Dubai Silicon Oasis filed its first corporate tax return at the end of year one. Net accounting profit for the taxable period: AED 590,000.

Two adjustments were applied before the rate ran:

+ AED 8,000 (municipality fines, non-deductible, added back) - AED 22,000 (exempt dividend income, removed)

Taxable income: AED 576,000

Running the numbers this way shows how to calculate corporate tax in UAE on an actual profit figure. Manual arithmetic works for planning. Accounting software reduces the risk of errors on your final corporate tax return.

Tax adjustments are where most calculation errors occur. Your accounting profit and taxable income will almost never be the same figure. The legal framework is designed to create that difference, and your corporate tax return must account for every part of it.

Under Ministerial Decision No. 73 of 2023, deductible expenses must directly relate to business activity and must not fall under a statutory exclusion. Applying that test to grey-area expenses is where most businesses need professional support.

Corporate tax deductible expenses in the UAE follow a business-relatedness test. If an item is partly personal and partly commercial, only the business portion qualifies. Document everything clearly.

Free zone entities sit fully within the scope of UAE corporate tax. They must still register, file, and maintain records. No entity-level exemption exists.

The distinction comes from Qualifying Free Zone Person (QFZP) status under the UAE Corporate Tax Law. A UAE corporate tax free zone business that satisfies the FTA's conditions, including substance requirements and qualifying income tests, may apply a 0% rate to that income stream. Non-qualifying income is taxed at 9%.

The QFZP regime grants a conditional rate on Qualifying Income. It does not remove your filing obligations or the requirement to meet substance conditions every taxable period.

Small Business Relief works like a highway toll bypass lane. Your revenue is the vehicle in this analogy. If it stays under AED 3 million for the taxable period, you are permitted to take the bypass. Zero toll applies until 31 December 2026, when the regulations reset.

To claim small business relief corporate tax UAE treatment, you file an election alongside your corporate tax return for the relevant taxable period. You have to make that claim actively. Revenue must not exceed AED 3 million for the period, and crossing that figure by any amount removes eligibility for that full year.

Three errors come up more often than any others when businesses work through their first corporate tax return.

Treating accounting profit as taxable income. The two figures are different by design. Tax adjustments exist to bridge them, and skipping this phase produces an inaccurate return.

Failing to add back non-deductible items. Traffic fines, penalties, and 50% of client entertainment costs must all be added back to accounting profit before the rate applies. Leaving them out understates your liability.

Assuming a five-year record retention rule. The UAE Corporate Tax Law requires seven years, not the five-year window many businesses carry over from VAT practice. That difference matters when the FTA requests supporting documentation.

Meeting UAE corporate tax filing requirements means submitting before your deadline. The FTA charges penalties for late filing whether or not any tax is owed.

Is UAE corporate tax calculated on revenue or profit?

It is calculated on taxable income, derived from net accounting profit after applying legal tax adjustments. Gross revenue is not the tax base.

When is the corporate tax return due in the UAE?

The deadline is nine months after the end of the taxable period. Businesses with a 31 December financial year must file by 30 September of the following year through the FTA's EmaraTax portal.

Can losses from a previous year reduce my corporate tax liability?

Yes. The UAE Corporate Tax Law permits prior-period losses to offset up to 75% of taxable income in future years, subject to continuity-of-ownership conditions.

Does registering in a free zone automatically lower my corporate tax rate?

No. QFZP status requires satisfying every FTA condition, including substance requirements, and one failed condition moves all income to the standard 9% rate.

VAT in Dubai is exactly 5%. One rate, applied uniformly across all seven emirates. No exceptions by location. But how much is VAT in Dubai as a business owner i...

Download the app and make your everyday

life more efficient*

* coming in late 2026